- IRS Publication 502 Rules: Under current tax codes, prescription weight loss medications are fully eligible for HSA/FSA spending, but only when prescribed to treat a diagnosed medical condition like obesity, diabetes, or hypertension. Cosmetic weight loss is strictly excluded.

- The Crucial LMN Document: A Letter of Medical Necessity (LMN) is administrative proof for your plan administrator. It must contain your diagnosis code (such as ICD-10 code E66.9 for obesity), clinical justification, treatment plan, and your doctor's credentialed signature.

- Straightforward Payment: Patients can use their HSA/FSA debit card directly at checkout on telehealth sites like Losing Weight RX. Alternatively, you can pay out-of-pocket and submit your itemized receipts for subsequent reimbursement.

- Know the Exclusions: Over-the-counter wellness supplements, gym memberships (unless backed by a disease-specific prescription and LMN), and regular foods or commercial meal deliveries are excluded under IRS rules.

- Flat-Rate Value: Telehealth weight loss protocols, including compounded GLP-1 medications, qualify for HSA/FSA coverage. Program fees, provider consultations, and expedited shipping are all covered.

- Appealing Denials: Claims are sometimes initially rejected due to simple administrative errors or missing documentation. Aligning diagnosis codes and submitting a physician-signed LMN typically resolves denials.

Introduction: Unlocking Tax-Free Dollars for Metabolic Health

The introduction of glucagon-like peptide-1 (GLP-1) receptor agonists, such as semaglutide and tirzepatide, has fundamentally transformed the field of chronic obesity care and metabolic medicine. Clinically proven to reduce body weight by 15% to over 20% in combination with lifestyle modifications, these medications address the hormonal and neurological pathways that govern satiety. However, the commercial pricing of brand-name GLP-1 therapies (exceeding $1,000 per month without insurance) remains a major barrier to care. Even when seeking affordable options like compounded semaglutide, patients look for ways to optimize their healthcare budgets. One of the most effective, underutilized mechanisms to offset these costs is using a Health Savings Account (HSA) or Flexible Spending Account (FSA).

While HSA and FSA programs allow you to pay for medical care using pre-tax dollars—effectively saving you 20% to 40% depending on your tax bracket—navigating the Internal Revenue Service (IRS) regulations can be complex. The IRS maintains strict standards regarding which treatments, services, and medications qualify as eligible medical expenses. To ensure your weight loss medication is covered, you must understand the rules of IRS Publication 502, the necessity of a Letter of Medical Necessity (LMN), and the exact administrative steps required for direct checkout or reimbursement. This comprehensive guide outlines the legal and clinical frameworks governing HSA/FSA usage for weight loss medications, helping you secure and maintain tax-free coverage for your metabolic health journey.

IRS Publication 502: The Baseline Legal and Tax Framework

To understand whether you can use pre-tax dollars for weight loss therapy, you must first examine the governing regulatory document: IRS Publication 502 (Medical and Dental Expenses). This publication defines what expenses can and cannot be deducted on federal income tax returns or reimbursed through tax-advantaged health accounts. The IRS definition of a qualifying medical expense is highly specific: it must be a payment made primarily for the prevention, mitigation, treatment, or cure of a physical or mental disease, or for the purpose of affecting any structure or function of the body.

Under these guidelines, the IRS draws a sharp, non-negotiable distinction between treatments designed to manage a diagnosed disease and those undertaken for general health, wellness, or cosmetic purposes:

- Diagnosed Medical Conditions (Eligible): If a physician diagnoses you with a chronic disease or metabolic condition, the clinical treatments prescribed to manage that condition are considered qualified medical expenses. This includes prescription weight loss medications (such as compounded semaglutide, compounded tirzepatide, Wegovy®, or Zepbound®), diagnostic blood work, and clinical consultation fees.

- Cosmetic and General Wellness (Excluded): If you seek weight loss therapy solely to improve your appearance or for general wellness without a specific medical diagnosis, the IRS strictly prohibits the use of HSA or FSA funds. The tax code explicitly states that expenses that are merely beneficial to general health are not deductible or reimbursable.

This legal distinction is supported by a major clinical shift in the wider medical community. In 2013, the American Medical Association (AMA) House of Delegates adopted Policy H-440.842, officially recognizing obesity as a multi-metabolic, progressive disease. This policy decision, backed by endocrinology and metabolic research, helped move obesity care away from the outdated "lifestyle flaw" model and establish it as a chronic disease. By recognizing obesity as a distinct medical disease, the AMA helped clear the path for clinical treatments to be categorized as essential medical care under tax law and insurance guidelines. Consequently, when a licensed clinician diagnoses a patient with obesity (ICD-10 code E66.9) or overweight with comorbidities (such as hypertension or type 2 diabetes), the treatment is no longer categorized as cosmetic or general health—it is a direct intervention for a chronic medical condition, qualifying it for HSA/FSA funding.

The Letter of Medical Necessity (LMN): Your Key to HSA/FSA Approval

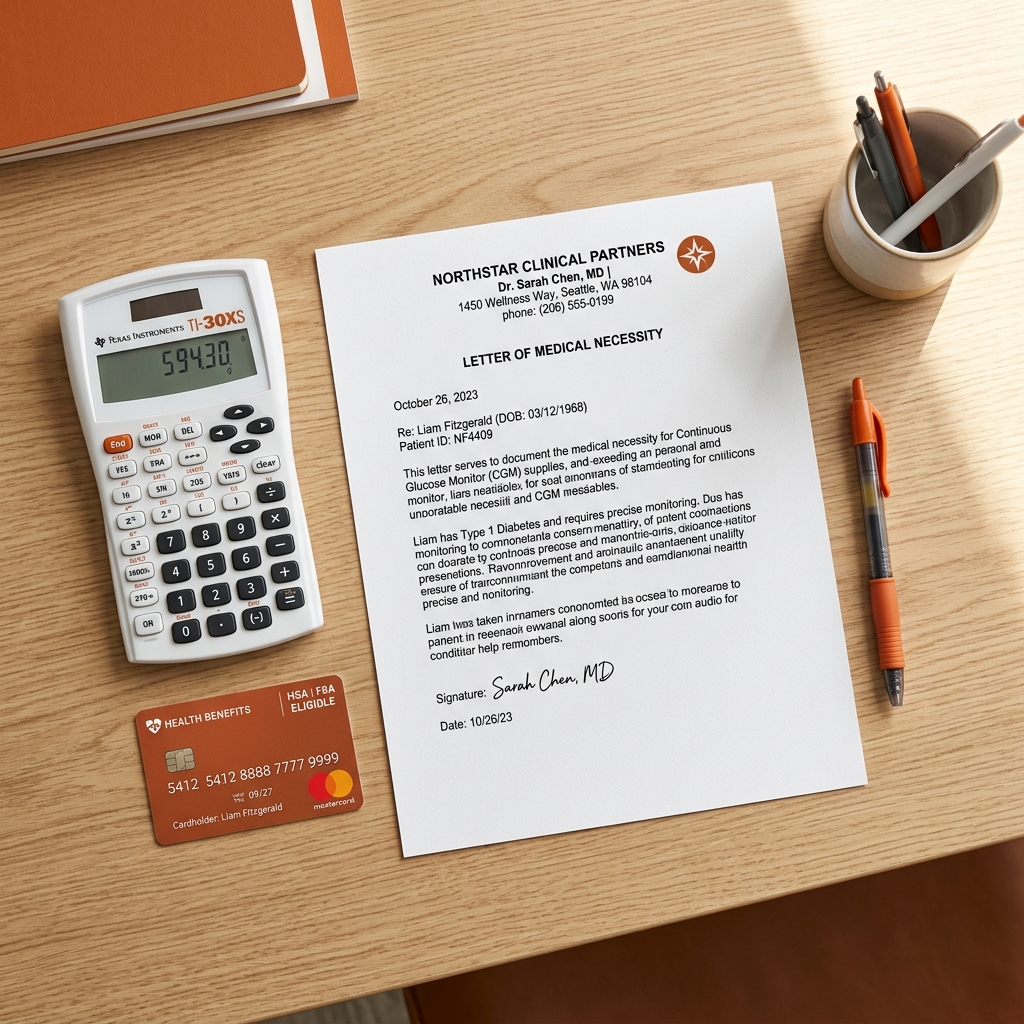

Because weight loss therapies can serve dual purposes—either treating a chronic disease or addressing cosmetic concerns—plan administrators require administrative proof of clinical need. This proof is provided through a document known as a Letter of Medical Necessity (LMN). An LMN is a formal clinical letter written and signed by a licensed healthcare provider, stating that a specific treatment is medically required to manage a diagnosed illness.

Without an LMN on file, third-party administrators (such as HealthEquity, Optum Bank, or WageWorks) will typically deny claims for weight loss medications, telehealth program subscriptions, or clinical support services. The LMN acts as the bridging link, proving to the administrator and the IRS that your expenditure conforms to the requirements of Publication 502.

A legally compliant and audit-ready LMN must contain several specific pieces of information:

- Patient Information: Your full legal name, date of birth, and plan member identification details. This must match the name on your health insurance, telehealth profile, and HSA/FSA account.

- Provider Credentials: The clinician's full name, medical license number, National Provider Identifier (NPI) number, practice address, and contact details.

- Specific Diagnosis Codes: The letter must state your specific medical diagnosis using standard International Classification of Diseases (ICD-10) codes. Common diagnostic codes for weight management include:

- ICD-10 E66.9: Obesity, unspecified (the primary diagnosis code for chronic weight management).

- ICD-10 E66.3: Overweight.

- ICD-10 E11.9: Type 2 diabetes mellitus without complications.

- ICD-10 I10: Essential (primary) hypertension.

- ICD-10 E78.5: Hyperlipidemia, unspecified (high cholesterol).

- Clinical Justification: The provider must outline your clinical indicators, such as your Body Mass Index (BMI), waist circumference, or metabolic blood panels. They should document why lifestyle modifications alone have been insufficient and why pharmacological intervention (such as a GLP-1 receptor agonist) is medically necessary to prevent further health deterioration.

- Clear Treatment Plan: The specific medication or protocol recommended (e.g., "Compounded Semaglutide Weight Management Protocol") and the anticipated duration of therapy.

- Clinician Signature and Date: A wet or verified electronic signature from your prescribing physician or nurse practitioner, along with the date of issue.

It is important to note that an LMN is not a permanent document. The IRS and health plan administrators generally require that a Letter of Medical Necessity be renewed annually (every 12 months). This ensures that your clinical team is actively monitoring your metabolic progress, checking for side effects, adjusting dosages, and confirming that ongoing pharmacological support remains medically appropriate for your health goals.

Below is a quick reference table showing which weight loss expenses are generally eligible for HSA/FSA reimbursement with a valid Letter of Medical Necessity, compared to those that are excluded under IRS rules:

| Expense Category | HSA/FSA Eligible (with LMN) | IRS Excluded (Non-Eligible) |

|---|---|---|

| Medications | Prescription GLP-1s, Compounded Semaglutide & Tirzepatide | Over-the-counter weight loss pills, fat burners, cosmetic compounds |

| Clinical Care | Doctor consultations, telehealth evaluation fees, lab panels | General health coaching (without medical oversight) |

| Nutrition & Diet | Nutritional therapy sessions with a registered dietitian | Regular food, weight loss meal deliveries, meal replacements |

| Fitness | Gym memberships prescribed to treat a specific disease (e.g., diabetes) | Standard gym memberships for general fitness, yoga classes |

| Equipment | Syringes, alcohol swabs, medical scale, blood pressure monitor | Fitness trackers, smartwatches, workout clothing |

HSA/FSA Eligible vs. Non-Eligible Items: Navigating the Nuances

To avoid plan rejections or tax penalties, you must understand the exact nuances of what you can purchase with your pre-tax funds. Even with a diagnosis of obesity and a signed LMN, some products and services remain strictly ineligible under IRS guidelines.

1. Prescription and Compounded Medications (Fully Eligible)

All prescription medications prescribed by a licensed medical provider to treat a diagnosed condition are qualified expenses. This includes brand-name GLP-1 medications (like Wegovy® and Ozempic®) and compounded options. For patients using telehealth programs like Losing Weight RX, the flat monthly fee ($146/mo for compounded semaglutide) is eligible because it directly represents the cost of the prescribed medication, clinical oversight, and delivery of medical supplies. If you want to compare prices to find the most cost-effective provider, you can review our guide to the cheapest semaglutide online in 2026 to maximize your HSA/FSA purchasing power.

2. Over-the-Counter Supplements (Generally Excluded)

The IRS maintains strict limits on over-the-counter (OTC) products. General vitamins, probiotics, herbal fat burners, and metabolism boosters are not eligible for HSA/FSA payment unless they are specifically prescribed by a physician to treat a diagnosed medical condition. For example, if a provider writes a prescription for a high-dose therapeutic vitamin to treat a diagnosed metabolic deficiency, it may qualify. However, purchasing generic wellness supplements at a retail pharmacy using your HSA/FSA debit card will usually result in a transaction decline or a documentation request from your administrator.

3. Foods and Meal Delivery Services (Strictly Excluded)

Perhaps the most common misunderstanding involves dietary foods, meal replacements, and specialized weight loss meal deliveries. Even if a doctor or registered dietitian strongly recommends a specific diet plan or meal prep service, the IRS explicitly excludes foods that satisfy normal nutritional needs. Under tax court precedents, food is considered a basic personal expense. The only exception is when the prescribed food is not part of normal nutrition and is used solely to treat an illness (such as special tube-feeding formulas). Standard commercial meal delivery programs or protein powders do not meet this standard, meaning they must be paid for out-of-pocket using post-tax dollars.

4. Gym Memberships and Fitness Equipment (Requires Stringent LMN)

A standard gym membership is generally considered a personal expense for general health and is not eligible. However, if you are diagnosed with a specific physical disease—such as severe obesity, hypertension, or type 2 diabetes—and your physician prescribes a structured exercise program at a gym as a direct treatment for that disease, the membership fees may become eligible. This requires a highly detailed LMN stating the diagnosis, the exact exercise protocol, and how it directly treats the illness. General fitness trackers, smartwatches, and athletic clothing remain non-eligible under all circumstances.

Start Compounded Semaglutide for $146/mo Flat-Rate

Use your HSA or FSA debit card directly at checkout. Our all-inclusive program features licensed provider evaluations, prescription medication, and sterile medical supplies shipped straight to your door.

Get Started TodayHow to Pay: HSA/FSA Checkout vs. Out-of-Pocket Reimbursement

Once you have confirmed that your clinical diagnosis and treatment plan meet IRS guidelines, you have two primary methods for paying for your weight loss medication: paying directly using your plan debit card or paying out-of-pocket and submitting a claim for reimbursement.

Method 1: Direct Payment Using Your HSA/FSA Debit Card

Most HSA and FSA plans issue a branded Visa or Mastercard debit card linked directly to your pre-tax account. This is the most convenient way to pay for your weight loss therapy:

- Check Card Balance: Ensure your HSA/FSA account has sufficient funds to cover the transaction before checkout. Unlike standard credit cards, HSA/FSA cards will immediately decline if the transaction amount exceeds your available balance.

- Enter Card Details: On telehealth platforms like Losing Weight RX, you can enter your HSA/FSA card number directly in the payment field at checkout. Because the platform specializes in clinical care, the transaction is categorized as a medical expense.

- Retain Documentation: Even if the charge is approved, your plan administrator may flag the transaction for verification. Always download the itemized invoice, medical intake summary, and prescription confirmation from your patient portal and save them in a dedicated folder.

Method 2: Pay Out-of-Pocket and Request Reimbursement

If you do not have an HSA/FSA debit card, or if your card is temporarily declined at checkout due to administrative flags, you can pay using a standard credit card and request reimbursement later:

- Pay with Personal Funds: Complete your checkout on Losing Weight RX using your personal credit card, debit card, or bank account.

- Obtain the Itemized Receipt: Log into your patient dashboard and download the itemized transaction receipt. To satisfy the IRS, the receipt must show: the patient's name, date of service, description of the clinical service or medication (e.g., "Compounded Semaglutide Prescribing & Medication"), provider details, and the exact amount paid.

- Submit the Claim Form: Log into your HSA/FSA provider portal, fill out their standard medical reimbursement claim form, upload your itemized receipt, and attach your signed Letter of Medical Necessity (LMN).

- Receive Tax-Free Funds: Once approved, the administrator will transfer the reimbursement directly to your linked personal bank account, tax-free.

Whether you choose direct payment or reimbursement, remember that the IRS requires you to maintain records of all HSA/FSA transactions for at least three years from the date you file your taxes. If you are audited, you must produce the itemized receipt, the prescription record, and the signed LMN for every transaction to prove the funds were used for qualified medical expenses. If you are exploring the safety profiles of compounded alternatives to ensure they align with your clinical requirements, refer to our detailed review on is compounded semaglutide safe.

What to Do If Your HSA/FSA Claim Is Denied

Receiving a denial notice from your HSA/FSA administrator can be frustrating, but it is a common part of the process. Administrators process millions of claims daily and often use automated screening programs that flag weight loss terms for manual review. In most cases, a denial is simply an administrative request for additional documentation rather than a final rejection of eligibility.

If your claim or transaction is denied, take the following steps to resolve the issue:

1. Verify the Diagnosis Code

A frequent reason for denial is that the submitted receipt or invoice does not clearly display an eligible ICD-10 diagnosis code. Review your itemized invoice to ensure it lists a code such as E66.9 (obesity) or E66.3 (overweight) alongside comorbidities. If the receipt only shows the charge amount without clinical context, request an itemized billing invoice from your provider’s support team.

2. Confirm Your LMN is Submitted and Active

If you used your HSA/FSA debit card and the transaction was approved but subsequently flagged, the administrator is waiting for your LMN. If you haven't submitted the letter, or if your LMN is older than 12 months, it is considered inactive. Obtain a current, signed LMN from your healthcare provider and upload it through your administrator's online portal to resolve the flag.

3. Check for Plan-Specific Forms

Some HSA/FSA administrators (such as Optum or WageWorks) require providers to complete the administrator's proprietary LMN form rather than accepting a generic clinical letter on letterhead. Log into your account, check the "Forms" section for a document titled "Letter of Medical Necessity Form" or "Dual-Purpose Expense Form," download it, and send it to your provider's support team for signature.

4. Submit a Formal Appeal

If the administrator officially denies your reimbursement request, you have the right to file an appeal. To do this, compile a comprehensive appeal package: your plan's appeal cover sheet, a copy of the denial letter, a letter from your doctor restating your diagnosis and the clinical necessity of the treatment, the original prescription, and your itemized receipt. Most appeals are approved once a clinical diagnosis code and clinician’s signature are provided. For a broader understanding of semaglutide protocols, dosages, and what to expect during treatment, read our complete guide to semaglutide.

Frequently Asked Questions

Yes. Under IRS Publication 502, prescription weight loss medications, including compounded semaglutide, are eligible for tax-free payment or reimbursement using HSA/FSA funds. However, they must be prescribed by a licensed healthcare provider to treat a diagnosed medical condition, such as obesity (ICD-10 E66.9) or type 2 diabetes, and cannot be used for cosmetic reasons.

A Letter of Medical Necessity (LMN) is a formal document from your healthcare provider stating that a specific treatment is medically required to treat a diagnosed disease. Under IRS rules, weight loss therapies are classified as "dual-purpose" expenses. Because they can be used for cosmetic purposes, an LMN is required to document that your treatment is clinically necessary to treat a disease, such as obesity (BMI over 30, or over 27 with comorbidities).

No. General over-the-counter (OTC) supplements, vitamins, and fat burners are strictly excluded from HSA/FSA eligibility by the IRS. Unless a supplement is explicitly prescribed by a licensed physician to treat a diagnosed medical condition, it does not qualify. General health and metabolic maintenance supplements do not meet the criteria of treating an active disease.

Yes, you can use your HSA/FSA debit card directly at checkout on the Losing Weight RX platform. Since our compounded semaglutide program includes provider evaluations and prescriptions, the transaction represents a medical expense. In case your plan administrator requests documentation, you can easily download your detailed itemized receipt and prescription records directly from your user dashboard.

If a claim is denied, first check that the diagnosis code (such as E66.9 for obesity) is clearly listed. Next, verify that your Letter of Medical Necessity (LMN) is on file with the administrator. Review if they require a specific form, and if needed, submit a formal appeal including your itemized receipt, the prescription, and your doctor's clinical justification.

Generally, no. The IRS explicitly excludes foods, diet shakes, and standard meal delivery services from HSA/FSA eligibility because they satisfy normal nutritional needs. Gym memberships and exercise programs are also excluded unless they are specifically prescribed by a physician to treat a diagnosed disease (like hypertension or diabetes) and accompanied by a detailed Letter of Medical Necessity.

Start Your Medical Weight Loss Program for $146/mo

Complete your online medical intake in minutes. If prescribed, receive compounded semaglutide shipped directly to your door. Pay securely using your pre-tax HSA or FSA debit card.

Start Assessment NowClinical References & Sources

- Internal Revenue Service. (2025). Medical and Dental Expenses (Including the Health Coverage Tax Credit) (IRS Publication 502). IRS Pub 502 PDF

- American Medical Association. (2013). Recognition of Obesity as a Disease. Policy H-440.842. AMA Policy Search

- Kyle, T. K., Dhurandhar, E. J., & Allison, D. B. (2016). Regarding obesity as a disease: The American Medical Association decision. Endocrinology and Metabolism Clinics of North America, 45(3), 511-520. PubMed Abstract